Redesigning the credit admin application workflow

Impact: Restructured credit workflows, improved data handoffs, reduced application processing time by 7%, and enhanced loan approval efficiency.

La Mesa RV's credit application was split across paper forms, AppOne, Dealertrack, and physical filing cabinets. Sales reps manually re-entered customer information into each system. Signed documents were stored locally and frequently lost.

The workflow enforced a fixed order that blocked deals whenever the process needed to flex, resulting in transcription errors at every handoff, no remote completion capability, and no integrated payments.

Design challenge

The redesign had to manage complex conditional logic across deal types, co-applicants, and optional steps. We needed to surface only relevant fields and actions, allow non-linear completion, and stay clear without breaking compliance.

System mapping

I mapped users, roles, and deal types to see where rigid workflows created bottlenecks. That clarified where flexibility was required and where constraints had to remain.

Non-linear flow

The existing process enforced a strict sequence that did not match real sales behavior. Teams needed to collect deposits early, skip steps when customers were present, or bypass credit checks for cash deals.

We shifted to a hub-and-spoke model so phases could complete in different orders while required dependencies still held. That aligned the system with how deals actually move.

Application flow

The workflow is organized into phases with flexible completion. Users can move between customer info, signatures, verification, and payments without breaking the process.

A stepper, auto-save, and non-blocking validation keep the experience guided without enforcing a rigid order.

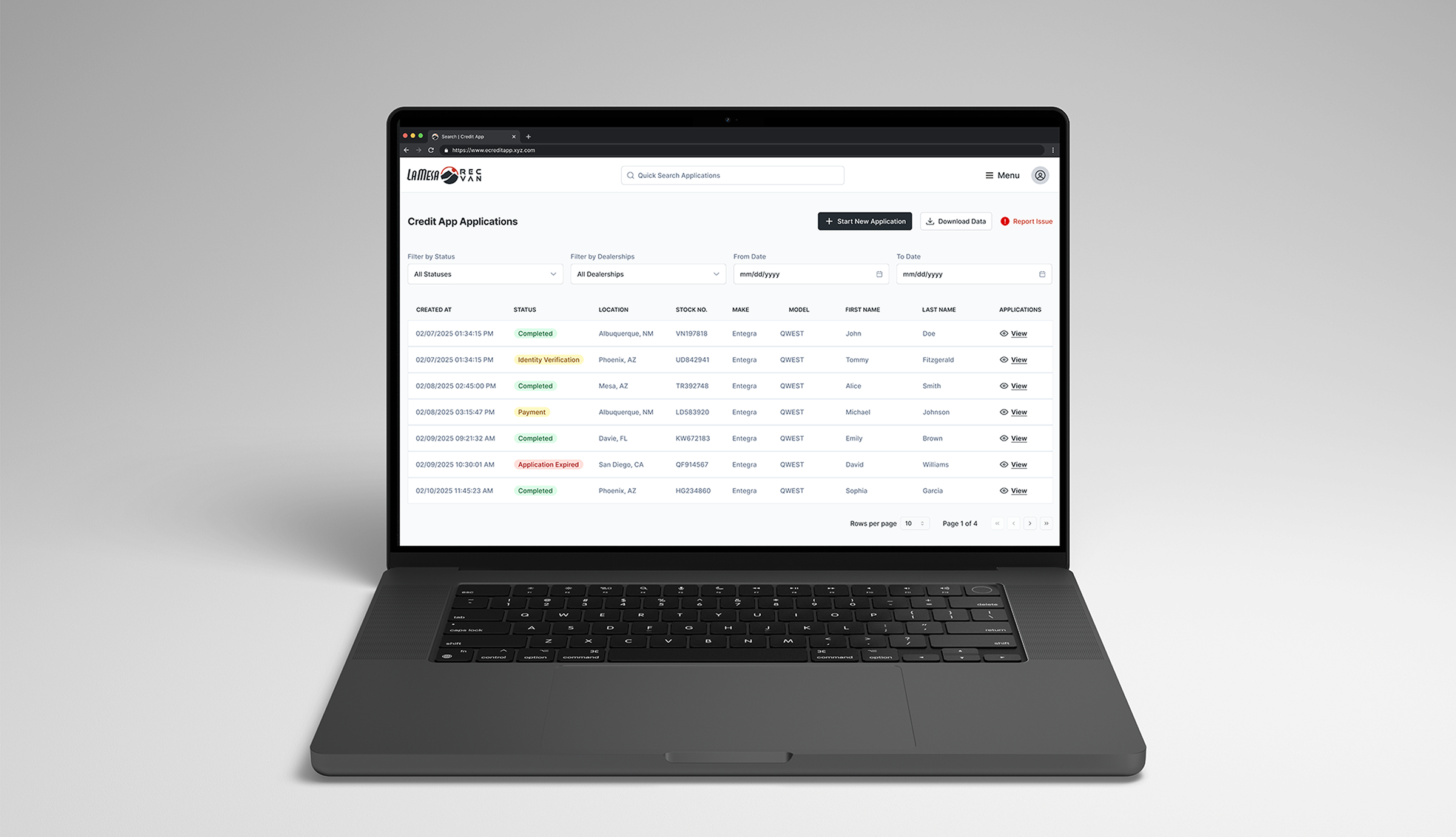

Admin dashboard

The dashboard gives a single overview of applications with the fields finance scans first, filters, and status indicators for quick decisions and reporting.

Action visibility

In the admin app, the key actions had been hidden until prerequisites were met, which created confusion. I made actions visible at all times and used state to show availability instead of hiding functionality.

That reduced uncertainty and helped users navigate complex workflows without feeling blocked.

Document access

Finance teams needed fast access to signed documents, but they were buried in the UI. I introduced a tab structure that elevated documents as a primary surface, cutting retrieval to two clicks.

Application locking

Applications lock after being sent to AppOne: fields become read-only with a clear system state. Admins can unlock when needed, balancing data integrity with flexibility and preventing errors after integration.

Locked applications use strong visual indicators and restricted editing so users understand final state and avoid corrupting data after external submission.

Integrations and technical ux

I designed around integrations. DocuSign handles signatures with real-time status, Stripe supports online and manual payments, and identity verification adapts to automated and in-person flows.

I accounted for async states and explicit system feedback so users always know what is happening behind the scenes.

Skip verification

For in person deals, sales can skip identity verification and move directly to payment. This was a tricky flow because it introduced the risk of bypassing an important compliance step while still needing to support real world sales behavior.

I designed a controlled skip flow with a confirmation step and full audit logging of who skipped and when, balancing speed for sales with accountability for finance.

Manual and online deposits

Deposit flows support both online and in-person transactions. Online payments attach receipts automatically; manual payments generate internal records. That reflects real dealership operations while keeping a clear audit trail.

Impact

Direct integration removed manual data re-entry. Documents are centralized and instantly accessible instead of being tracked down on paper.

Flexible workflows reduced friction and improved deal processing time. Integrated payments added traceability and simplified financial tracking, reducing processing time by 7% through improved interaction patterns and cleaner data handoffs.